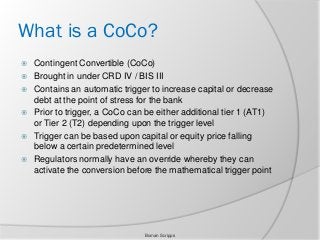

A CoCo, or enhanced capital note (ECN), is a kind of bond that may be converted into equity upon the occurrence of a certain event. CoCo is a term that has been debated extensively in the context of crisis management in the banking sector. It is also becoming more common as an alternate method of ensuring financial stability in the insurance sector.

What Exactly Are Cocos (Contingent Convertibles)?

Debt instruments known as Contingent Convertibles (CoCos) are commonly issued by banks in Europe. When used, contingent convertibles function similarly to standard convertible bonds. A bond's conversion into equity or stock occurs when its strike price is achieved. CoCos rely heavily on private banks and wealthy individuals in Europe and Asia for funding. CoCos are a popular investment vehicle in Europe due to their high yield and high risk. These investments are also known as capital improvement notes (ECN). The issuing financial institution can better weather a capital loss thanks to the hybrid debt securities' unique alternatives.

Banks may employ these instruments to strengthen their balance sheets since they enable them to convert debt into shares under certain capital requirements. The purpose of contingent convertibles was to aid undercapitalized banks and forestall another financial catastrophe like the one that occurred in 2007-2008. Banks in the United States have yet to adopt the usage of CoCos. Preferred stock is not how American banks raise capital.

Understanding Contingent Convertibles

Contrast bank-issued contingent convertibles with standard or plain vanilla convertible debt offerings. As with traditional bonds, convertible bonds pay interest on a set schedule and rank higher than unsecured creditors in the event of company bankruptcy or insolvency. To further benefit from the rising value of the underlying shares, bondholders might convert their debt holdings into common shares at a predetermined strike price. To initiate the conversion, the stock price must reach the strike price. When the stock price of a firm is rising, convertible bonds may be converted into shares of stock, providing a profit for investors. Due to the convertible feature, investors may reap the advantages of bonds with a set interest rate and the opportunity for capital growth from a growing stock price.

However, unlike standard convertible bonds, contingent convertibles allow for more flexible conversion terms. Bondholders, like holders of other types of debt instruments, are paid a predetermined interest rate at regular intervals during the course of the bond's term. These bank-issued subordinated debts are convertible into common stock according to the same conditions as convertible bonds. The event may be triggered in a variety of ways, such as when a certain threshold is reached in the underlying shares of the institution, when the bank is required to fulfill regulatory capital requirements, or when the demand is made by management or supervisory authorities.

Benefits and Risks for Investors

Increased demand for contingent convertibles may be attributed to their high yield in a market saturated with safer, lower-yielding alternatives. The issuing banks have benefited from the increased stability, and capital flow brought about by this expansion. Although the risk is larger than usual, many investors are willing to take it because they believe the bank will eventually repurchase the debt.

The bank determines the conversion rate at which investors obtain common shares. The financial institution is free to set the conversion price of the shares at the same level as when the debt was issued, the market price upon conversion, or any other level. A potential drawback of stock conversion is that it dilutes the value of existing shares, which lowers profits per share.

Additionally, the investor may be required to keep the CoCo for a significant amount of time since there is no assurance that the CoCo will ever be completely redeemed or converted to equity. It may be difficult for investors to sell or unwind a CoCo investment since regulators that permit banks to issue CoCos want their banks to be well-capitalized. If authorities do not permit the sale of CoCos, investors may have trouble unloading their holdings.

Pros

- CoCo bonds are a way for European banks to obtain Tier 1 capital.

- The bank has the option of deferring interest payments or even canceling the loan altogether if required.

- High-interest payments are made on a regular basis, which is far higher than the interest rate on conventional bonds.

- The value of an investor's shares rises if and only if a CoCo is triggered by a rise in the stock price.

Cons

- If the bonds are converted to stock, the investors will incur the risks and have little input.

- If investors own bank-issued CoCos that have been converted to stock, they will likely get shares at a lower price.

- If authorities do not permit the sale of CoCos, investors may have a hard time unloading their holdings.

- To attract investors, banks and firms issuing CoCos must provide a larger interest rate than is typical for bonds.

Conclusion

Investors in CoCo bonds should consider the possibility that they may need to take swift action in the event that the bonds are converted. They risk major losses if they don't act. Buying the stock upon the occurrence of the CoCo trigger may not be optimal for a number of reasons, as was previously mentioned.